By Wenqi Huang, Brighton Jones, and Obioha Okereke, College Money Habits

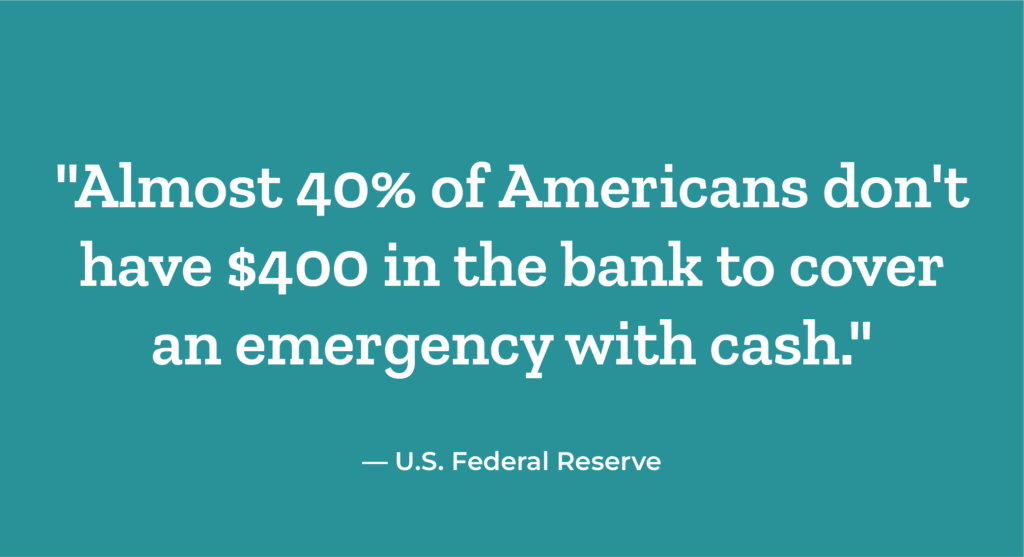

An emergency fund, as the name suggests, is an account where you put away savings for emergency situations. Unforeseen events happen around us all the time and when situations do arise, we want to be prepared to face them financially.

Some examples of when you might need to tap into an emergency fund include unemployment, unplanned medical expenses, home or car repairs, etc. There are many different guidelines on how much to save for an emergency fund. A simple way to look at it is:

- Set aside three months of fixed and variable expenses if you have two sources of sizable income — either through employment, alimony, inheritance, etc. or married with both spouses working.

- Set aside six months of fixed and variable expenses if you only have one source of income.

Just as with any goals you make, it takes time to incrementally achieve your target. Start with setting a goal, then with each paycheck, move a set amount into a separate account that you have opened specifically for this purpose.

An emergency fund should be easily accessible and kept liquid, in other words, in cash or readily available to convert into cash without a major sacrifice to its market price. If it makes sense for you, consider opening a high-yield interest savings account for the funds to accumulate some interest (often higher than traditional banks) while you are not using the funds. Other options include a checking or savings accounts, money market accounts, or a certificate of deposit that matures within a year.

Once the emergency fund account has accumulated your target savings, you can stop putting money into that account and put it towards another savings goal. However, as money in the emergency account gets withdrawn for emergency expenses, make sure to refill it in preparation for the next unforeseen event.

Calculating the Size of Your Emergency Fund

The most common guidance around emergency funds is to set aside three to six months of living expenses. This is so in the event of an unexpected life change, you will be able to afford to pay for your basic necessities and bills without running out of money or requiring a loan.

To calculate how much you need, start by calculating your living expenses. This will include costs such as:

- Rent/mortgage

- Groceries

- Utilities

- Transportation

- Insurance

- Loan payments

You’ll want to add all of these to calculate the total of your monthly living expenses. Once you’ve calculated the cost of your living expenses, you’ll want to multiply by 3 or 6 to arrive at the recommended amount for your emergency fund.

For instance, if the total cost of your living expenses is $3,000, then you might set a goal of saving $18,000 for your emergency fund.

This would represent six months of living expenses and ensure that if you were to suddenly lose your job, or experience an unexpected medical expense, you could afford to cover your basic needs for the next 6 months.

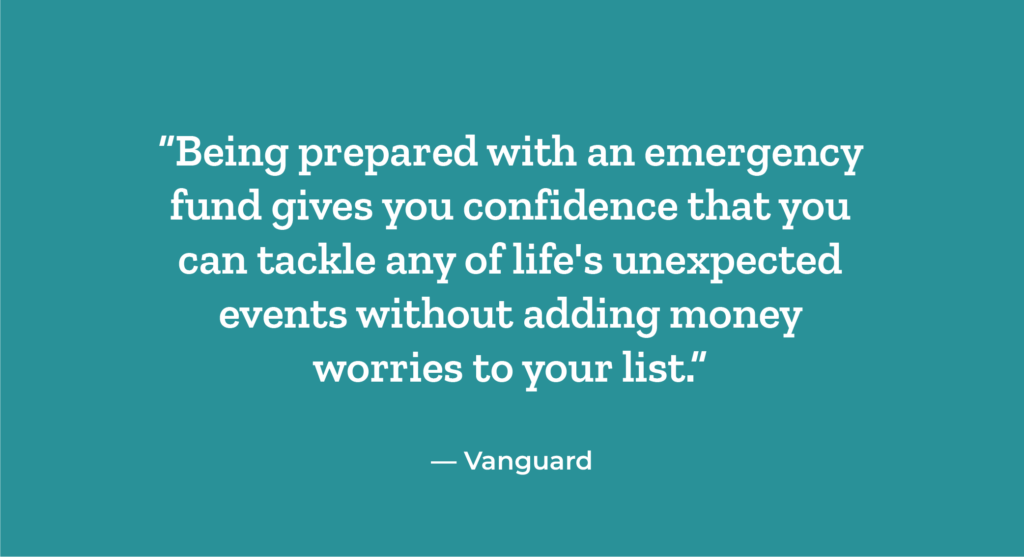

Financial Security

In addition to providing temporary financial stability if something unexpected occurs, an emergency fund gives you more financial confidence.

If it seems unrealistic to save three to six months’ worth of living expenses, set a smaller goal. For instance, instead of focusing on setting aside three months of living expenses, you might start with saving one month of living expenses.

Also, when you set a goal of establishing an emergency fund, make sure to track your progress and stay consistent with your savings efforts. If you are planning on purchasing a home or a vehicle soon, build an emergency savings fund that enables you to deal with maintenance or repair costs too, as these can suddenly become necessary and be expensive.

If you have any questions regarding these personal finance resources and/or general questions about managing your personal finances, contact Obi Okereke from College Money Habits at learn@collegemoneyhabits.com.

Related Articles:

Four Ways to Boost Your Savings

Savings provide financial security and enable you to pursue your passions. Start on the path to financial freedom by adopting these four strategies to amass savings.

Retirement Planning: How to Start

Learning the importance of planning for retirement and ways to build a retirement plan can help you pursue your lifestyle goals in the future.

Setting Financial Goals

Understanding your values and your financial goals create a framework for financial health — helping you prioritize how you spend your money and stay accountable.

Blog | How Saving and Investing Impacted My Life

College Money Habits Founder Obioha Okereke shares three of the biggest money habits that changed his life.