By Obioha Okereke, College Money Habits

Over the past 25 years, I have learned many lessons when it comes to personal finance. During that time, I have made mistakes, had successes, and I’ve been forced to make some tough decisions.

Over the past 25 years, I have learned many lessons when it comes to personal finance. During that time, I have made mistakes, had successes, and I’ve been forced to make some tough decisions.

Here are three of the biggest money habits that have changed my life.

1. Automate Your Savings

During college, frustrated with the lack of interest I was earning on my savings, I ended up closing my savings account and transferring the funds to my checking account. For the next few years, all the money I earned went into my checking accounts or into investments.

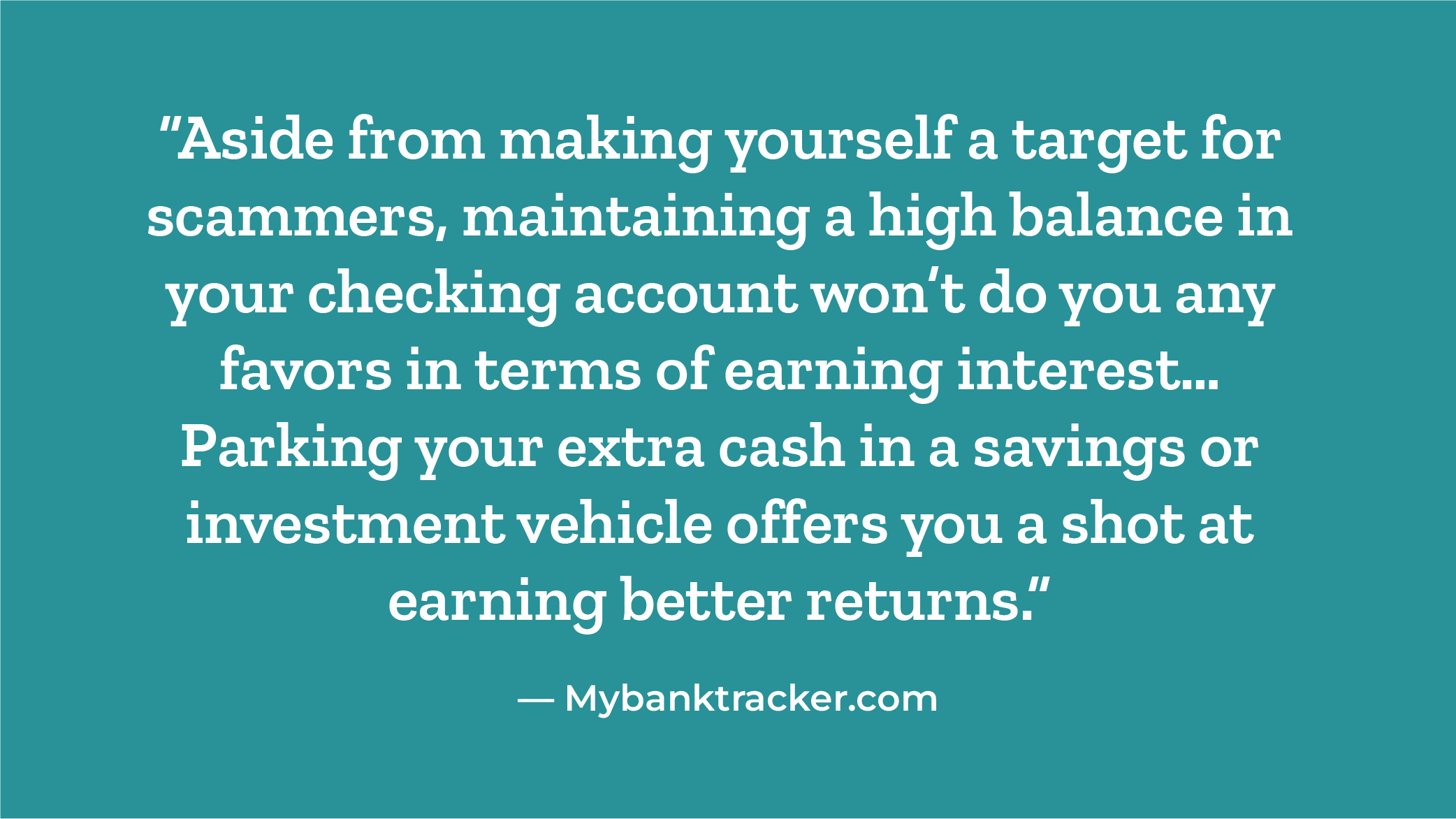

Was this a wise strategy? Not quite. Due to inflation, I was losing money by keeping a high balance in my checking account — due to the rising cost of goods, money loses roughly 3% on average of its value every year.

At the end of 2020, I opened a high-yield savings account through Ally Bank. When I set up my account, I set up an automatic transfer of $1,250 to make sure that regardless of what happened in my life, every month I would be setting aside some money. A few lump sum transfers and 1.5 years later, my savings account now has a little over $37,000 in it. During that time, I also earned over $100 in interest. Yes, this might not seem like a lot but it is a lot more than $0, which is what I was earning when the money was in my checking account.

Automating my savings also forced me to budget around saving. The monthly $1,250 transfer occurred at the beginning of every month, and it was my responsibility to make sure there was enough money in my checking account for the transfer to occur. By having this automatic transfer, I was encouraged to consider it an “expense” along with my other bills. In considering saving as an expense, it became mandatory for me and, in turn, helped me consistently set money aside.

If you are looking to increase your savings, I can’t emphasize enough how beneficial automating your savings can be. Start with something small and make sure that it does not impact your overall budget, then slowly increase the amount over time. Not only does this help you boost your savings, but is an extremely effective way of building an emergency savings fund and makes managing your money less stressful.

2. Start Investing

I started investing when I was a senior in high school and to be honest, it might be the best decision I have ever made. My only regret was that when I started, I did not have a strategy and I was not as consistent as I should have been.

My first investment was in a total stock market index fund — an investment vehicle that tracked the performance of the overall stock market. My investment was $150.

Over the years, I invested in Starbucks, Amazon, Microsoft, and numerous other companies. Then, at the age of 24, after six years of investing, my portfolio reached $100,000.

When it comes to investing, time is the most important factor. The earlier you start, the longer your money has time to grow and compound. I made it a habit to invest regularly into my 401k, an employer sponsored retirement account, or one of my individually managed accounts and, in doing so, helped me slowly build my portfolio over time.

Tip: Before you start investing, create an emergency savings fund. Investing carries risk and because you have the potential to lose money, it is critical that you have money set aside in case the value of your investments decrease.

3. Delay Gratification

During college and even now that I have graduated, I have always had the same mentality: t I am willing to sacrifice now to ensure that in the future, I can live comfortably, have fun with my family, and do all the things I enjoy. To stay true to this, I have had to make tough decisions.

One of my favorite phrases and one that I’ve come to live by is, “That is not in my budget right now.”

I got used to saying “no” to vacations, “no” to going out on the weekends, and refrained from spending my money frequently on dining out or purchasing expensive clothing that I did not need. I started practicing these habits when I was earning $18,000 a year working part-time in retail.

There is a popular quote that says something to the effect of, ‘If you don’t know how to manage $1,000, you won’t be able to manage $10,000,” and I completely agree. Had I never learned to exhibit self-control and postpone purchasing everything I wanted when I was growing up, it would be extremely difficult to manage my spending now that I am earning more.

I went from earning roughly $20,000 per year to earning $100,000 per year in just over 12 months. Due to my discipline in learning the difference between “needs” versus “wants” and knowing the importance of looking long term, it has been so much easier to manage my spending.

I do think it is extremely important to spend money on the things you enjoy because honestly, what else is the money for? Nevertheless, it is paramount that you plan ahead when spending and consider the long-term impacts of financial decisions you make now.

By living a very conservative lifestyle growing up, I am now in a position where I can afford not only to live comfortably, but also pursue goals I used to dream about.

So, if I can pass on anything to you, it is this: live for today, but plan for the future too.

If you have any questions regarding these personal finance resources and/or general questions about managing your personal finances, contact Obi Okereke from College Money Habits at learn@collegemoneyhabits.com.

Related Articles:

Four Ways to Boost Your Savings

Savings provide financial security and enable you to pursue your passions. Start on the path to financial freedom by adopting these four strategies to amass savings.

What is an Emergency Savings Fund?

An essential part of financial health is creating an emergency savings fund to tap for unanticipated expenses, like medical bills or job loss. Learn how to save for emergencies.

Retirement Planning: How to Start

Learning the importance of planning for retirement and ways to build a retirement plan can help you pursue your lifestyle goals in the future.

Setting Financial Goals

Understanding your values and your financial goals create a framework for financial health — helping you prioritize how you spend your money and stay accountable.