By Kaleb Strawn, Brighton Jones, and Obioha Okereke, College Money Habits

It can often feel stressful and overwhelming to think about your finances all at once. When you consider the rent payment that is due at the end of the month, the credit card debt you are trying to pay off, the savings you want to build for a down payment on a home, and the dollars you are trying to invest for retirement — this is all enough to make your head spin.

You may find yourself wondering, where do I begin? How do I get started? What takes priority?

Fortunately, this is where setting clear financial goals can help provide clarity and actionable steps toward achieving the ultimate intentions you have with your money.

What Are Financial Goals?

Financial goals are the objectives that you want to achieve with your money during a specified time frame. These objectives can be short-term or long-term in nature.

Short-term goals are what you want to achieve within three years. Examples of short-term goals could be:

- Create and follow a budget.

- Save a certain amount for an emergency or rainy-day fund.

- Pay off your credit card debt.

Long-term goals are what you want to achieve further in the future. Examples of long-term goals could be:

- Save money for children’s educational needs.

- Save for a special trip.

- Pay off your mortgage.

- Save enough to retire comfortably.

Ultimately, you will want to have a clear idea of both your short-term and long-term goals so you can create an actionable plan to accomplish them.

Why Should You Set Financial Goals?

Setting financial goals is the first step towards becoming financially secure. Specifically, establishing financial goals will help you become accountable. They will help you prioritize things that are important to you, and they will allow you to measure and celebrate progress.

Accountable: Writing down your financial goals can help you stay accountable. This will help provide a clear picture of what you are trying to accomplish and why you work hard to earn the money that you do. With constant access to your ultimate goals, the temptation to needlessly spend will become increasingly easier to resist and help you to stay on track.

Prioritize: Your goals should be unique and tailored to what is important to you. You will want to rank your goals in order of their importance and necessity to your specific situation. It is important to be realistic and ensure you are ticking off the goals that could have immediate consequences if not addressed. For instance, you should prioritize paying off high-interest-rate-bearing debt prior to remodeling the bathroom.

Measure and Celebrate Progress: You will want to periodically measure your progress toward your goals. As you find yourself inching closer to the goals you have set out for yourself, excitement will start to build which will only motivate you more to cross that finish line. And when you do, celebrate! Take time to celebrate your successes and all the hard work you have put in to getting where you are.

How to Create Financial Goals

When you are in the process of creating your financial goals, it’s helpful to establish SMART goals. You may have heard of this acronym before, it stands for specific, measurable, achievable, realistic, and time-based.

Specific: Make sure your goal is not too vague. Specific goals make it easier to understand what you are trying to achieve and how you will go about achieving it.

For example, instead of saying “I’d like to save more money”, set a goal of setting aside an additional $100 every month into a savings account.

Measurable: Quantify your goals so they can be easily tracked.

It is important to have measurable goals because this is how you can determine whether or not your goals have been accomplished. If your goal is to save more money, ask yourself the following questions:

- How much would I like to save?

- What is the end goal?

- How much can I afford to save?

- When would I like to accomplish this?

- What challenges might I face and are there things I can do to plan for them?

With any goal you have, it is key to clearly state what you hope to accomplish. This will help keep you focused and encouraged to follow your plan. The more measurable the goal, the easier it will be to determine success.

Achievable: You will want to make sure your goal is achievable and not set your aspirations too high. It may help to start with smaller steps towards a larger goal.

Keep in mind, while it is important to set goals, if you set too many, or are overly ambitious, this can lead to feelings of dissatisfaction and disappointment. It can be tempting to set lofty goals. First, start by trying to set measurable goals that are realistic. Let’s walk through an example.

Unrealistic Goal: I would like to save $50,000 by the end of the year.

Realistic Goal: I will save $50,000 over the next two years by setting aside $1,200 every month and contributing $100 per month to my investments.

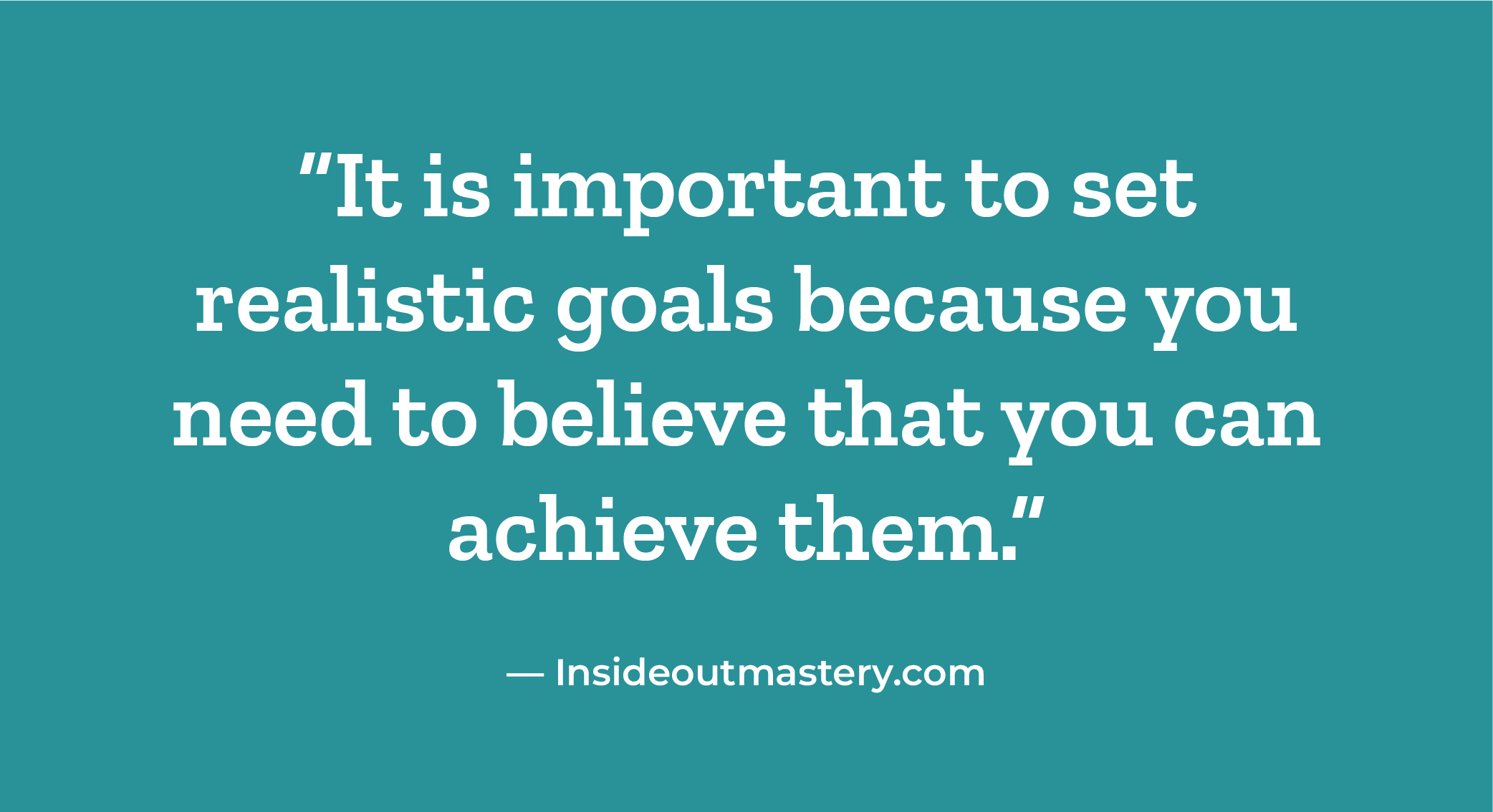

The real advantage of setting realistic, achievable goals is that they inspire you to act.

If you set goals that you don’t believe you can achieve anytime soon, you may feel less motivated to pursue them. So, while a goal might be challenging and require sacrifices, it should not be impossible.

Relevant: Ask yourself, why am I setting this goal? Think about your overall financial picture and if this goal will help you achieve your ideal scenario.

A real-life example, a goal of mine has been to purchase a property, either to live in, or to use as a rental property. My original goal was to purchase a property by the end of 2021. However, due to astronomically high real estate prices and a family situation, I had to ask myself “Is this the right time?”

I had never lived without my parents before and was not familiar with all the costs associated with owning a residence and being financially independent. In the end, I decided to rent an apartment with my brother. I do not regret my decision because if I had purchased a property at the time, I most likely would not have the financial flexibility I have today.

When setting relevant goals, it is paramount for you to evaluate if you will benefit from the goal or if it could have adverse impacts on your financial well-being .

Time-based: Your goal should have a beginning and end date. If you do not present a deadline for yourself, you may become less motivated to accomplish your goal.

Setting goals should be fun! Remember, if you don’t meet one of your goals by your target date, this doesn’t mean you’ve failed. Life happens, emergencies happen. What is important however, is that you stay consistent and focused on the long-term.

Lastly, don’t forget to celebrate every win! You deserve to reward yourself for all you’ve achieved. It is easy to get into a habit of continuously setting new goals, chasing larger achievements and forgetting to enjoy the small things. Remember to pause, take a step back, and look at all you’ve accomplished.

Now, go set some new financial goals. You’ve got this!

If you have any questions regarding these personal finance resources and/or general questions about managing your personal finances, contact Obi Okereke from College Money Habits at learn@collegemoneyhabits.com.

Related Articles:

Four Ways to Boost Your Savings

Savings provide financial security and enable you to pursue your passions. Start on the path to financial freedom by adopting these four strategies to amass savings.

What is an Emergency Savings Fund?

An essential part of financial health is creating an emergency savings fund to tap for unanticipated expenses, like medical bills or job loss. Learn how to save for emergencies.

Retirement Planning: How to Start

Learning the importance of planning for retirement and ways to build a retirement plan can help you pursue your lifestyle goals in the future.

Blog | How Saving and Investing Impacted My Life

College Money Habits Founder Obioha Okereke shares three of the biggest money habits that changed his life.