By Obi Okereke, College Money Habits

We often hear about the importance of budgeting and saving money, but sometimes this feels easier said than done. Fortunately, it is never too late to create a budget!

As you think about creating a budget, or modifying your current one, here are five common mistakes you can avoid:

1. Not Creating A Budget

Not having a budget can lead to overspending or make it difficult to plan for the future.

Building a budget encourages you to understand your income and expenses. It provides a framework to set short-term and long-term goals, manage your money, and plan ahead. Creating and following a budget can also boost your confidence when it comes to making financial decisions because you will have a clearer understanding of your money.

That said, creating a budget is only half the battle! Sticking to your budget is just as important as creating one.

Want to create a budget? Start by figuring out your discretionary income and writing down your short-term and long-term goals.

Interested in learning more? Check out How to Create a Personal Budget.

2. Not Tracking Your Spending

If you do not track your spending, it is hard to know where your money is going.

Tracking your spending involves keeping tabs on your expenses, such as rent, food, clothing, and utilities. Every dollar should be accounted for!

Why is tracking your spending important? Let’s say that you review your spending for the month and find you are spending half of your total income on food. In general, food expenditures should be about 10 to 15 percent of monthly take-home pay. This might mean you need to change your menu planning or where you shop to reduce spending on food — and allow for more of your money to go toward other expenses or savings.

“When budgeting for food, you should plan to spend a minimum of $250 per adult, and $150 per child each month. For example, a family of four with two children should budget $800 per month.” – Be The Budget

Don’t have time to record every expense? There are plenty of budgeting apps and resources that make it easy to keep track of where your money is going. Applications like Mint, You Need a Budget, and Honeydue will automatically record all your spending via debit and credit cards, allocate them into different categories, and notify you when you have exceeded your budget. Additionally, these resources let you add investment accounts, retirement accounts, loans, and other assets, such as vehicles, giving you a holistic picture of your net worth and financial picture.

Don’t know your net worth? Figure it out using the Net Worth Calculator.

3. Guessing About Your Expenses

If you were to ask the total amount of your monthly expenses, would you know the answer?

A very common mistake when it comes to budgeting is guessing your expenses, instead of tracking them. When you guess the total cost of your expenses, it is challenging to recognize how much of your income you can actually save.

Often, you will be surprised by your spending when you compare it to your expectations. An important part of building your confidence around your finances is understanding where your money is going.

For example, let’s say that you earn $3,000 a month in net income; this means, every month, after you have paid taxes, you are left with $3,000. If your expenses total $2,500, this means you have the ability to save $500 every month. However, if you don’t identify your total expenses, it can become difficult to understand how much money you have left over at the end of every month and how it can be budgeted.

If you do not actively track your expenses and simply “guess” as to where your money is going, you will have no idea how much money you can save every month.

Start by looking at and totaling your previous month expenses. Calculate what percentages of your income you are spending on food, housing, transportation, fun, etc. and compare to recommended percentages. You might find that you are spending more than you are making, or with small changes to your spending you could be saving monthly.

Once you begin tracking your expenses, it becomes easier to set parameters around your spending and keep yourself accountable. If you find that you are regularly overspending in one area, you might set a goal to reduce your spending in that category by $100 per month. Now, every month, you can look at your spending and quickly assess if you have improved or not.

4. Not Budgeting for Fun

Life does not need to be boring! When putting together a budget, make sure to allocate some of your spending for the things you enjoy.

If you’re a foodie and want to try a new restaurant every month, budget for it. Want to take a vacation? Budget for that too.

If you do not budget for “fun” you will likely end up overspending. Budgeting will allow you to enjoy the things you love, with the people you love, while never having to worry about if you can afford it or not.

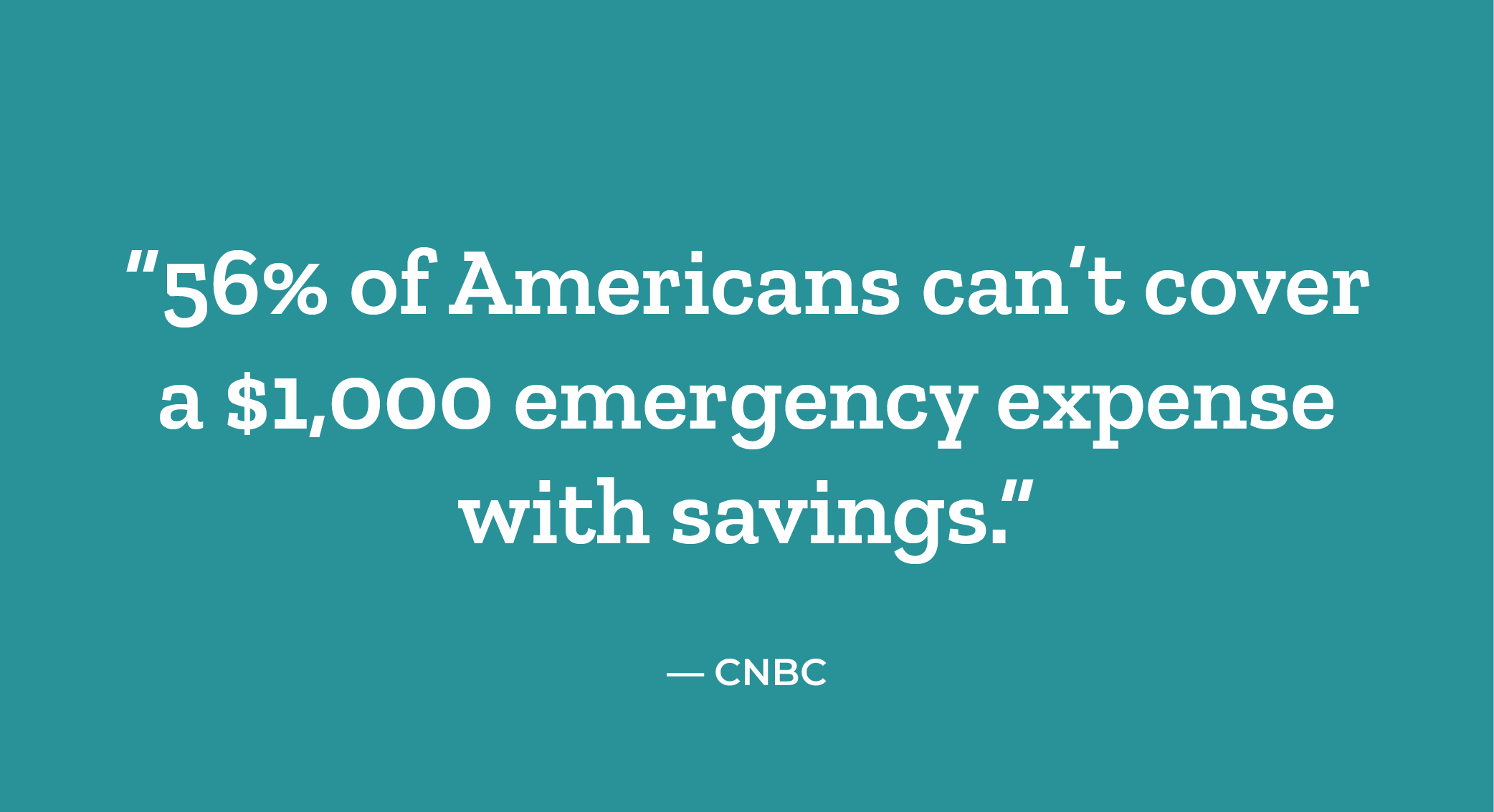

5. Not Creating an Emergency Fund

Given the current economic climate, it is more important than ever to make sure you are always setting money aside in an emergency savings fund.

What is an emergency fund? An emergency fund is money set aside to deal with unexpected events, such as job loss, medical expenses, or other sudden emergencies. By creating an emergency savings fund, you create a buffer that you can tap into when life gets crazy.

To create an emergency savings fund, you want to set aside 3 to 6 months of living expenses. So, if your total monthly expenses for necessities (rent/mortgage, utilities, phone, food, etc.) is $3,000, then you would want to set aside anywhere from $9,000 to $18,000.

If you do not set up an emergency fund, you might be forced to take out a loan, or request money from family or friends when dealing with unexpected emergencies.

To get started, try setting a goal of saving an additional $100 a month. By the end of the year, you’ll have $1,200! While this might not reflect 3 to 6 months of living expenses, it is a healthy beginning to building your savings.

Put something away now and you’ll thank yourself later!

Now that you know some of the most common budget mistakes, you know what to avoid as you go about creating a plan for your future.

As you work towards building better money habits, remember that it is a learning experience and that mistakes happen! Take it day by day and make sure you are setting goals and holding yourself accountable.

If you have any questions regarding these personal finance resources and/or general questions about managing your personal finances, contact Obi Okereke from College Money Habits at learn@collegemoneyhabits.com.

Related Articles:

Understanding Discretionary Income

Budgeting starts with knowing your discretionary income. Learn what goes into calculating it and apps to help you track spending against your budget.

How to Create a Personal Budget

Take charge of your financial health by following these six steps to create your own budget based on your discretionary income and spending.

The 50-30-20 Budget

This popular budgeting strategy helps you manage your money with 50% for needs, 30% for wants, and 20% for saving, investing and/or paying off deb

Blog | 3 Money Lessons that helped me save $100,000

College Money Habits Founder Obioha Okereke describes three important money habits that gave him the confidence and skills to save $100,000.